The 4% Rule: A Simple Guide to Retirement Withdrawals

Retirement is a time to enjoy the fruits of your labor, but it also comes with the challenge of making your savings last. One of the most widely discussed strategies…

Tip: save now, read later.Retirement is a time to enjoy the fruits of your labor, but it also comes with the challenge of making your savings last. One of the most widely discussed strategies for managing retirement funds is the 4% rule. This rule provides a straightforward approach to withdrawing money from your retirement accounts while minimizing the risk of running out of funds. In this article, we’ll explore what the 4% rule is, how it works, its pros and cons, and how you can apply it to your retirement planning.

What Is the 4% Rule?

The 4% rule is a retirement withdrawal strategy designed to help retirees sustainably manage their savings. It suggests withdrawing four percent of your retirement portfolio in the first year of retirement and adjusting the amount each subsequent year for inflation.

For example, if you have a 1 million portfolio, you would withdraw 1 million portfolios, and you would withdraw 40,000 in the first year. If inflation is 2% the following year, you will withdraw 40,800(40,800(40,000 + 2%). This approach aims to provide a steady income stream while preserving your savings for 30 years or more.

Financial advisor William Bengen popularized the rule in the 1990s based on historical market data and retirement scenarios. While it’s not a one-size-fits-all solution, it remains a useful starting point for retirement planning.

This rule can be used for your Retirement Financial Security.

How Does the 4% Rule Work?

The 4% rule is based on a few key assumptions:

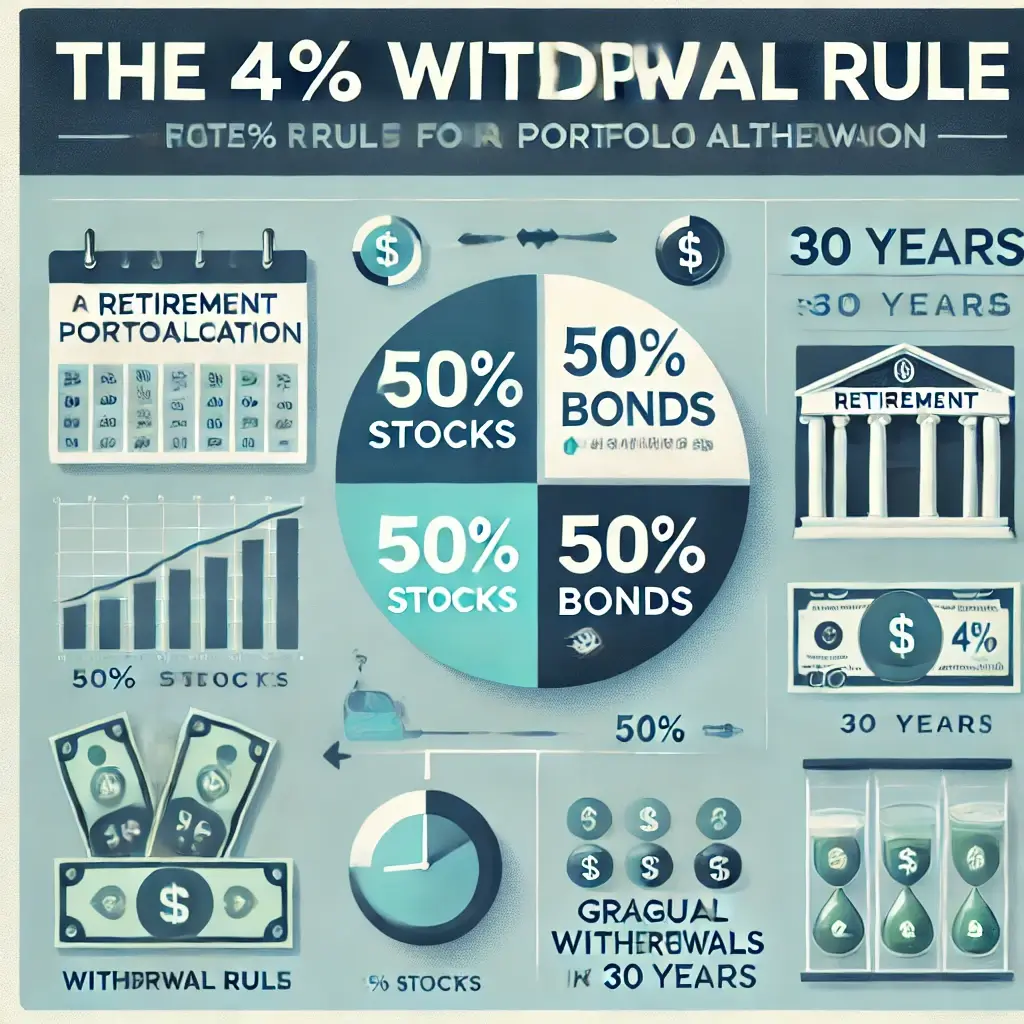

- Portfolio Composition: A balanced portfolio of 50% stocks and 50% bonds.

- Time Horizon: A retirement period of 30 years.

- Inflation Adjustment: Annual withdrawals adjusted for inflation.

By following these guidelines, the 4% rule aims to balance the need for income with the goal of preserving your savings. It’s designed to withstand market fluctuations and ensure your money lasts throughout retirement.

Pros of the 4 percent Rule

- Simplicity: The 4% rule is easy to understand and implement, making it accessible for most retirees.

- Predictability: It provides a clear withdrawal framework, helping you plan your retirement budget.

- Historical Success: Based on past market performance, the rule has a high success rate for 30-year retirements.

- Flexibility: You can adjust the rule to suit your needs, such as withdrawing less during market downturns.

Cons of the percent Rule

- Market Dependency: The rule assumes average market returns, which may not hold true in the future.

- Inflation Risks: High inflation can erode your purchasing power over time.

- Longevity Risk: If you live longer than 30 years, you may outlast your savings.

- One-Size-Fits-All: The rule doesn’t account for individual circumstances, such as healthcare costs or lifestyle changes.

How to Apply the 4% Rule to Your Retirement

- Calculate Your Portfolio Size: Determine the total value of your retirement savings, including 401(k)s, IRAs, and other investments.

- Determine Your Withdrawal Amount: Multiply your portfolio value by 4% to find your first-year withdrawal amount.

- Adjust for Inflation: Increase your withdrawals annually to account for inflation.

- Monitor Your Portfolio: Regularly review your investments and adjust your strategy as needed.

For example, if you have 1.5 million in retirement savings, your first−year withdrawal would be 1.5 million in retirement savings, and your first-year withdrawal would be 60,000. If inflation is 3% the next year, you would withdraw $61,800.

When the 4 percent Rule Might Not Work

While the 4% rule is a helpful guideline, it may not be suitable for everyone. Here are some scenarios where you might need to adjust your approach:

- Early Retirement: If you retire before age 65, you may need to withdraw less to make your savings last longer.

- High Healthcare Costs: Retirees with significant medical expenses may need to reduce withdrawals to cover these costs.

- Market Volatility: During economic downturns, consider withdrawing less to protect your portfolio.

- Luxury Lifestyle: If you plan to travel extensively or pursue expensive hobbies, you may need to save more or withdraw less.

Alternatives to the 4% Rule

If the 4% rule doesn’t align with your goals, consider these alternatives:

- Dynamic Withdrawals: Adjust your withdrawals based on market performance. For example, withdraw less during downturns and more during upswings.

- Bucket Strategy: Divide your portfolio into “buckets” for short-term, medium-term, and long-term needs.

- Annuities: Use annuities to provide a guaranteed income stream, reducing reliance on market performance.

- Hybrid Approach: Combine the 4% rule with other strategies to create a customized plan.

Conclusion: Is the 4% Rule Right for You?

The 4% rule is a valuable tool for retirement planning, offering a simple and effective way to manage your savings. However, it’s not a one-size-fits-all solution. Your retirement needs, lifestyle, and financial goals will determine whether this strategy works for you.

To make the most of the 4% rule, regularly review your portfolio, stay informed about market trends, and adjust your plan as needed. By combining the 4% rule with other strategies, you can achieve retirement financial security and confidently enjoy your golden years.

FAQs About the 4% Rule

1. Can I withdraw more than 4% in retirement?

Withdrawing more than 4% increases the risk of running out of money, especially if markets underperform. Stick to 4% or less for long-term sustainability.

2. What if my portfolio grows significantly after I retire?

If your portfolio grows, you can reassess your withdrawals. Some retirees increase their spending or leave a larger legacy for their heirs.

3. Does the 4% rule work for early retirees?

Early retirees may need to withdraw less than 4% to ensure their savings last longer. Consider a 3% or 3.5% withdrawal rate for extended retirements.

4. How does the 4% rule account for taxes?

The 4% rule doesn’t factor in taxes. Be sure to account for taxes when calculating your withdrawals to avoid unexpected shortfalls.