Budgeting 101: How to Create a Budget That Actually Works

Budgeting isn’t about restriction—it’s about control, freedom, and financial security. In this guide, you’ll learn:✅ Why most budgets fail (and how to avoid those mistakes)✅ Step-by-step instructions to build a budget that works✅ Proven budgeting methods (pick…

Tip: save now, read later.Budgeting isn’t about restriction—it’s about control, freedom, and financial security. In this guide, you’ll learn:

✅ Why most budgets fail (and how to avoid those mistakes)

✅ Step-by-step instructions to build a budget that works

✅ Proven budgeting methods (pick the best one for your lifestyle)

✅ Tips to stick to your budget (without feeling deprived)

Do you feel like your money disappears before the month ends? Are you tired of living paycheck to paycheck? If so, you’re not alone—many people struggle with managing their finances. The good news? A well-structured budget can change everything.

New in budgeting see our guide on to budget for every stage of life.

Let’s dive in and transform your financial future—starting today.

Section 1: Why Most Budgets Fail (And How to Fix It)

Before we build a budget that works, let’s understand why most fail:

1. Unrealistic Expectations

Many people set extreme budgets (e.g., “I’ll only spend $50 on eating out this month!”)—then give up when they overspend.

✅ Fix: Start with small, flexible limits and adjust as needed.

2. Not Tracking Expenses

If you don’t know where your money goes, you can’t control it.

✅ Fix: Use apps like Mint, YNAB, or a simple spreadsheet to track every dollar.

3. Ignoring Irregular Expenses

Forgotten costs (car repairs, holidays, subscriptions) wreck budgets.

✅ Fix: Create a “sinking fund” for unexpected or annual expenses.

4. No Emergency Fund

Without savings, emergencies force debt.

✅ Fix: Save $1,000 ASAP, then build 3-6 months’ expenses.

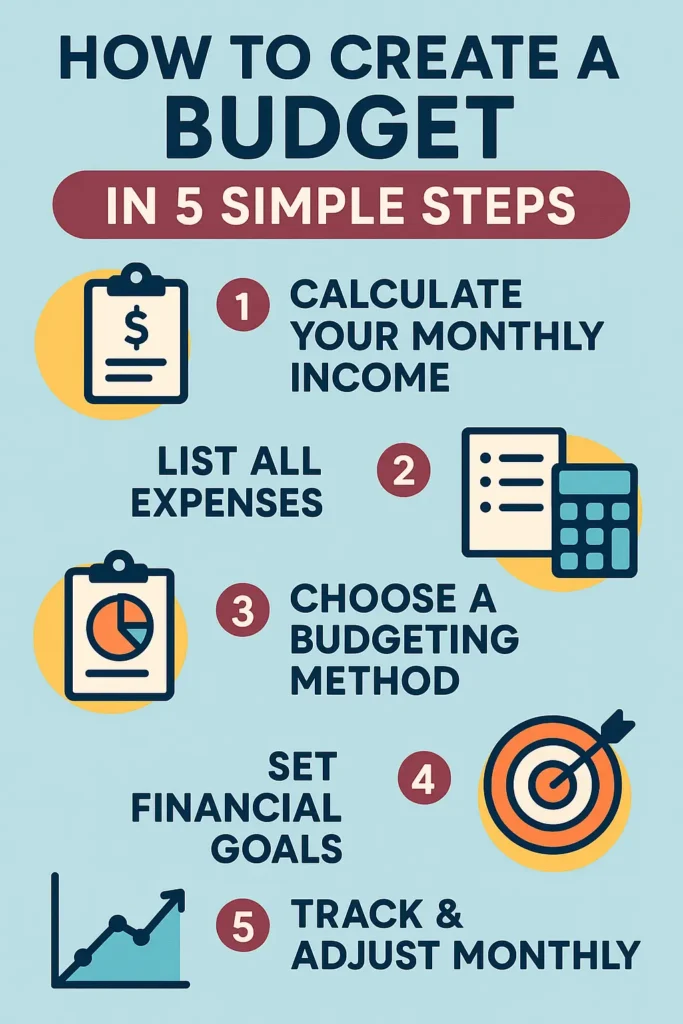

Section 2: How to Create a Budget in 5 Simple Steps

Step 1: Calculate Your Monthly Income

Begin by determining your total monthly income, which includes all sources such as your salary, bonuses, freelance work, and any passive income streams. This foundational step is crucial as it sets the stage for understanding how much money you have available to allocate towards expenses and savings.

Include:

- Salary (after taxes)

- Side hustles

- Passive income

❌ Mistake: Budgeting with gross (pre-tax) income.

Step 2: List All Expenses

Next, compile a comprehensive list of all your expenses. Categorize them into fixed expenses, like rent or mortgage payments, and variable expenses, such as groceries and entertainment. This detailed overview will help you understand where your money is going each month.

Fixed Expenses:

- Rent/mortgage

- Utilities

- Insurance

Variable Expenses:

- Groceries

- Entertainment

- Dining out

Irregular Expenses:

- Car maintenance

- Gifts

- Subscriptions

✅ Pro Tip: Review 3 months of bank statements to catch hidden spending.

Step 3: Choose a Budgeting Method

After identifying your income and expenses, select a budgeting method that suits your lifestyle. Popular approaches include the envelope system, zero-based budgeting, or the 50/30/20 rule. Each method has its own advantages, so choose one that aligns with your financial goals and habits.

Pick one that fits your lifestyle:

A. 50/30/20 Budget

- 50% Needs (rent, bills, groceries)

- 30% Wants (dining, hobbies)

- 20% Savings/Debt

✅ Best for: Beginners who want flexibility.

B. Zero-Based Budget

- Every dollar has a job (even savings).

- Example: If you earn 3,000∗∗,allocateall∗∗3,000∗∗,allocateall∗∗3,000.

✅ Best for: Detail-oriented planners.

C. Cash Envelope System

- Use cash only for categories like groceries and entertainment.

✅ Best for: Overspenders (forces discipline).

Step 4: Set Financial Goals

Establish clear financial goals to guide your budgeting process. Whether you aim to save for a vacation, pay off debt, or build an emergency fund, having specific targets will motivate you to stick to your budget and make informed spending decisions.

Examples:

- Short-term: Save $500 emergency fund

- Mid-term: Pay off $2,000 credit card debt

- Long-term: Save for a house down payment

✅ Pro Tip: Use SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound).

Step 5: Track & Adjust Monthly

Finally, make it a habit to track your spending and adjust your budget monthly. Regularly reviewing your financial situation allows you to identify areas for improvement and adapt to any changes in income or expenses, ensuring that your budget remains effective and relevant.

- Weekly check-ins (avoid surprises)

- Monthly reviews (adjust categories as needed)

✅ Tool Recommendation: YNAB (You Need a Budget) helps with real-time adjustments.

Section 3: How to Stick to Your Budget (Without Going Crazy)

1. Automate Savings & Bills

- Set up auto-transfers to savings.

- Use auto-pay for bills to avoid late fees.

2. Use the “24-Hour Rule” for Non-Essential Purchases

Wait 24 hours before buying—avoid impulse spending.

3. Reward Yourself (Responsibly)

Example: If you stay under budget for 3 months, treat yourself to a small splurge.

4. Try a No-Spend Challenge

- 7-day no-spend challenge (only essentials).

- Helps reset spending habits.

5. Find an Accountability Partner

Share goals with a friend or spouse—motivation boosts success.

Section 4: Advanced Budgeting Tips

1. Negotiate Bills

- Call providers (internet, insurance) to lower rates.

2. Meal Planning = Huge Savings

- Saves $200+/month vs. eating out.

3. Use Cashback Apps

- Rakuten, Honey, Ibotta give free money back.

4. Annual Subscription Audit

Cancel unused gym memberships, streaming services.

5. Increase Income (Side Hustles)

- Freelancing, Uber, tutoring—extra $500/month helps!

Conclusion: Your Budget = Your Financial Freedom

Budgeting isn’t about deprivation—it’s about making your money work for you. By following these steps, you’ll:

✔ Stop living paycheck to paycheck

✔ Build savings & crush debt

✔ Gain peace of mind

Action Step: Start today—open a spreadsheet or budgeting app and track your last month’s spending. Small steps lead to big wins!