Beef stew is the ultimate comfort food. This hearty beef stew recipe brings tender chunks of beef, soft vegetables, and a rich savory broth together in one warm bowl. It’s cozy, flavorful, and perfect for chilly nights. With simple ingredients and slow cooking, it’s a recipe you’ll crave all winter.

Versatile: Works in stovetop, slow cooker, or Instant Pot.

Family-friendly: A dish everyone will enjoy.

Ingredients

Yields 6 servings

2 pounds beef chuck, cubed

3 tbsp olive oil

2 medium onions, chopped

3 cloves garlic, minced

4 medium carrots, sliced

3 celery stalks, chopped

3 medium potatoes, cubed

3 tbsp tomato paste

4 cups beef broth (low sodium)

1 cup red wine (or extra broth)

2 tbsp Worcestershire sauce

2 tsp salt

1 tsp black pepper

2 tsp dried thyme

2 bay leaves

2 tbsp flour (for thickening)

For Garnish

Fresh parsley, chopped

Extra black pepper

💡 Tip: Swap red wine with Guinness for a richer flavor or add mushrooms for extra depth.

Step-by-Step Instructions

Step 1: Prepare the Beef

Pat beef dry with paper towels. Season with salt and pepper. Heat 2 tablespoons of olive oil in a large pot or Dutch oven. Brown the beef in batches, about 4–5 minutes per side. Set aside.

Step 2: Sauté the Vegetables

Add remaining oil to the pot. Cook onions, carrots, and celery for 5 minutes until softened. Stir in garlic and tomato paste. Cook 1 minute more.

Step 3: Build the Base

Add wine (if using) and scrape up brown bits from the pot. Let simmer 2–3 minutes. Stir in broth, Worcestershire sauce, thyme, bay leaves, and browned beef.

Step 4: Simmer the Stew

Bring to a boil, then reduce heat. Cover and simmer 1½ to 2 hours, stirring occasionally. The beef should be tender.

Step 5: Add Potatoes

Stir in potatoes. Cook for another 30 minutes until potatoes are fork-tender.

Step 6: Thicken and Serve

Remove bay leaves. Mix flour with a few tablespoons of broth in a small bowl to create a slurry. Stir into stew. Simmer until thickened. Garnish with fresh parsley. Serve hot.

Slow Cooker Method

Brown beef as above.

Add beef, vegetables, broth, wine, and seasonings to the slow cooker.

Cook on LOW for 8–9 hours or HIGH for 4–5 hours.

Add slurry near the end to thicken.

Instant Pot Method

Brown beef on Sauté mode. Remove.

Sauté onions, carrots, and celery. Add garlic and tomato paste. Deglaze with wine.

Add beef back with broth, potatoes, and spices.

Pressure cook on High for 35 minutes. Natural release 10 minutes.

Chef’s Tips for Perfect Beef Stew

Use the right cut: Beef chuck has enough fat for tender results.

Brown well: Deep browning gives maximum flavor.

Don’t rush: Low and slow makes beef melt-in-your-mouth.

Deglaze: Scrape up browned bits — they’re flavor gold.

Rest time: Stew tastes even better the next day.

Variations to Try

Guinness Beef Stew: Replace wine with Guinness for rich depth.

Herb Boost: Add rosemary and bay leaves for earthy aroma.

Mushroom Stew: Stir in mushrooms during the last 30 minutes.

Gluten-Free: Skip flour and thicken with cornstarch slurry.

Serving Suggestions

Pair this hearty beef stew with:

Crusty bread or buttery rolls

Mashed potatoes for an extra cozy meal

A crisp green salad for balance

Storage and Freezing

Refrigerate: Up to 4 days in airtight container.

Freeze: Up to 3 months. Thaw overnight in the fridge.

Reheat: Warm gently on stovetop, adding a splash of broth if needed.

Nutrition (per serving)

Calories: ~420

Protein: 34 g

Fat: 20 g

Carbs: 28 g

Fiber: 4 g

Frequently Asked Questions

Everything you need to know about making the perfect beef stew.

What cut of beef is best for stew?

Beef chuck is ideal because it has the right balance of fat and connective tissue.

It becomes tender and flavorful after slow cooking. Brisket and short ribs also work well.

Can I make beef stew without wine?

Yes. Replace red wine with extra beef broth for a non-alcoholic version.

A splash of balsamic vinegar adds depth of flavor if desired.

How do I thicken my beef stew?

Mix 1–2 tablespoons of flour or cornstarch with cold water to make a slurry.

Stir it into the stew and simmer until thickened. You can also mash a few potatoes.

Can I freeze beef stew?

Yes. Beef stew freezes well for up to 3 months.

Cool completely before freezing. Reheat gently on the stovetop, adding broth if it thickens too much.

Why does stew taste better the next day?

Resting allows flavors to meld and deepen overnight.

Store it in the fridge and reheat slowly for the best results.

Final Thoughts

This hearty beef stew recipe is the perfect comfort food for winter nights. With tender beef, flavorful vegetables, and a rich broth, it’s a recipe that will warm your table and your heart.

Prefer something with bold and savory flavors? Try our Black Pepper Chicken recipe — it’s peppery, satisfying, and just as comforting as a classic beef stew.

White chicken chili soup is creamy, comforting, and lightly spicy. It relies on tender chicken, white beans, green chiles, aromatics, and warm spices. Unlike red chili, it uses chicken broth instead of tomatoes. The result is a hearty, soup-like bowl that still tastes like chili.

This soup blends chili technique with soup texture. You sweat onions and garlic. Then you bloom spices. Next you simmer shredded chicken with white beans and green chiles in broth. Finally, you finish with creaminess for body and balance.

Ingredients

Yields 6 hearty bowls

2 tbsp olive oil

1 medium onion, diced

3 cloves garlic, minced

2 cans (4 oz each) diced green chiles, mild

2 tsp ground cumin

1 tsp ground coriander

1 tsp dried oregano

1/2 tsp chili powder (or ancho)

4 cups low-sodium chicken broth

2 cans (15 oz each) cannellini or great northern beans, rinsed

3 cups cooked shredded chicken (rotisserie works)

1/2 tsp kosher salt, to taste

1/4 tsp black pepper

1/2 cup sour cream (or Greek yogurt)

4 oz cream cheese, softened (optional, for extra creaminess)

Juice of 1/2 lime

Toppings

Fresh cilantro, chopped

Sliced jalapeño (optional)

Shredded Monterey Jack or pepper Jack

Crushed tortilla chips

Avocado slices

Substitutions: Use navy beans for a thinner body, or add 1/2 cup corn for sweetness. Swap sour cream with Greek yogurt for higher protein.

Step-by-step instructions for White chicken chili soup

Sweat aromatics. Heat olive oil in a pot over medium heat. Add onion. Cook for 4–5 minutes. Stir in garlic. Cook 30 seconds.

Bloom spices. Add cumin, coriander, oregano, and chili powder. Stir 30–45 seconds until fragrant.

Build the base. Add green chiles and broth. Bring to a gentle boil.

Add beans and chicken. Stir in beans and shredded chicken. Reduce to a lively simmer. Cook 12–15 minutes.

Make it creamy. Lower heat. Whisk in sour cream and cream cheese until smooth. Do not boil after dairy goes in.

Balance. Stir in lime juice. Taste and adjust salt and pepper.

Serve. Ladle into bowls. Add toppings.

Slow cooker option

Add onion, garlic, spices, green chiles, beans, chicken, and broth to the slow cooker.

Cook on LOW 5–6 hours or HIGH 2.5–3 hours.

Stir in sour cream, cream cheese, and lime at the end. Heat 10 minutes more without boiling.

Instant Pot option

Sauté onion and garlic on Sauté. Bloom spices 30 seconds.

Add green chiles, beans, chicken, and broth. Seal and cook 8 minutes (Manual/Pressure). Natural release 10 minutes.

Switch to Sauté (Low). Stir in sour cream, cream cheese, and lime. Heat gently.

Chef’s tips

Do not boil dairy. Keep the finish silky by warming gently.

Thicker body. Mash 1 cup of beans and stir back in.

Spice control. Use hot green chiles or add cayenne for heat.

Deeper flavor. Add 1 tsp chicken bouillon powder if your broth is mild.

Freshness. Lime juice at the end brightens the pot.

Corn + cilantro. Stir in 1 cup corn during the last 5 minutes.

No-dairy light version. Skip dairy; blend 1 cup soup and return for body.

Turkey swap. Use leftover turkey after holidays.

Extra protein. Stir in 1 cup cooked quinoa at the end.

Serving ideas for White chicken chili soup

Serve with warm tortillas or cornbread.

Add a simple green salad with lime vinaigrette.

Offer a toppings bar for a crowd.

Love this cozy bowl? For another comforting classic, see

(Creamy Tortellini Soup).

It features tender cheese tortellini in a velvety broth—perfect alongside your White Chicken Chili Soup.

Storage and freezing

Fridge: 4 days in airtight containers.

Freeze: Up to 2 months. For best texture, freeze before adding dairy; add after reheating.

Reheat: Low heat on stove; add broth if too thick.

Nutrition (estimate per serving, 1/6 of recipe)

~390 kcal; 31 g protein; 18 g fat; 26 g carbs; 5 g fiber; 900 mg sodium (varies with broth, dairy, and toppings).

Troubleshooting

Too thin? Simmer uncovered 5–10 minutes or mash beans.

Too thick? Add warm broth in small splashes.

Grainy dairy? Heat gently and whisk; avoid boiling.

Flat flavor? Add 1/4 tsp salt and more lime.

Frequently Asked Questions

Quick answers to common questions.

Can I use raw chicken instead of cooked?

Yes. Simmer 1 lb raw chicken breasts in the broth for 12–15 minutes until 165°F (74°C). Rest, shred, and return to the pot before adding dairy.

How do I make it spicier?

Use hot green chiles, add 1 diced jalapeño with the onions, or stir in 1/8–1/4 tsp cayenne at the spice-blooming step.

Can I make it dairy-free?

Yes. Skip sour cream and cream cheese. Blend 1 cup of the soup and stir it back to thicken naturally. Finish with extra lime.

Will it freeze well?

Best practice is to freeze before adding dairy. Reheat gently, then add sour cream and cream cheese. If freezing leftovers with dairy, thaw in the fridge and reheat very gently to avoid curdling.

How can I thicken the soup?

Mash 1 cup beans and stir back, simmer uncovered 5–10 minutes, or add a small slurry (1 tsp cornstarch + 1 tbsp cold water), then simmer briefly.

Make-ahead plan

Cook up to step 4 the day before. Chill quickly. Reheat on low, then add dairy and lime right before serving to keep it silky.

Cost saver tips related to White chicken chili soup

Use dry beans you cook ahead.

Buy family-pack chicken and freeze in portions.

Swap pepper Jack with Monterey Jack on sale.

White Chicken Chili Soup

Prep:Cook:Total:Yield:6 servings

Ingredients

2 tbsp olive oil

1 medium onion, diced

3 cloves garlic, minced

2 cans (4 oz) diced green chiles, mild

2 tsp ground cumin

1 tsp ground coriander

1 tsp dried oregano

1/2 tsp chili powder (or ancho)

4 cups low-sodium chicken broth

2 cans (15 oz) white beans, rinsed

3 cups cooked shredded chicken

1/2 tsp kosher salt, to taste

1/4 tsp black pepper

1/2 cup sour cream (or Greek yogurt)

4 oz cream cheese, softened (optional)

Juice of 1/2 lime

Tip: For extra body, mash 1 cup of beans and stir back in.

Instructions

Warm oil in a pot over medium heat. Sauté onion 4–5 minutes. Add garlic 30 seconds.

Stir in cumin, coriander, oregano, and chili powder; bloom 30–45 seconds.

Add green chiles and broth; bring to a gentle boil.

Stir in beans and chicken. Simmer 12–15 minutes.

Lower heat. Whisk in sour cream and cream cheese until smooth. Do not boil.

Finish with lime juice, salt, and pepper. Serve hot with toppings.

Slow cooker: Add everything except dairy and lime; cook LOW 5–6 h or HIGH 2.5–3 h. Stir in dairy + lime to finish.

Chef’s Notes

Spice: Add diced jalapeño with onion, or a pinch of cayenne with the spices.

Thickness: Simmer uncovered a few minutes, or mash some beans.

Freezing: Best to freeze before adding dairy; stir dairy in after reheating.

Nutrition (per serving)

~390Calories

31 gProtein

18 gFat

26 gCarbs

5 gFiber

Estimates only. Values vary with ingredients and toppings.

Pumpkin bread is a fall favorite. Cinnamon swirl pumpkin bread mini loaves take the classic recipe to the next level. They are moist, flavorful, and perfectly portioned. These loaves make excellent snacks, gifts, or additions to holiday tables. The sweet cinnamon swirl inside adds a delightful surprise in every bite.

Why You’ll Love Cinnamon Swirl Pumpkin Bread Mini Loaves

Perfect for fall: The combination of pumpkin and cinnamon captures autumn’s essence.

Mini size: Great for portion control, gifting, or sharing.

Moist and tender: Pumpkin purée keeps the loaves soft for days.

Customizable: Add nuts, chocolate chips, or a glaze to make them unique.

Make-ahead friendly: Freeze them for quick treats later.

Ingredients You’ll Need

Here’s a complete list of ingredients for this recipe:

1 ¾ cups all-purpose flour

1 teaspoon baking soda

½ teaspoon baking powder

1 teaspoon ground cinnamon

½ teaspoon ground nutmeg

½ teaspoon ground ginger

½ teaspoon ground cloves

½ teaspoon salt

1 cup pumpkin purée (not pumpkin pie filling)

½ cup vegetable oil (or melted butter)

¾ cup granulated sugar

½ cup brown sugar, packed

2 large eggs

1 teaspoon vanilla extract

For the cinnamon swirl:

½ cup brown sugar

1 tablespoon ground cinnamon

Step-by-Step Directions

Preheat oven: Set to 350°F (175°C). Grease four mini loaf pans or line with parchment.

Mix dry ingredients: In a bowl, whisk flour, baking soda, baking powder, spices, and salt.

Combine wet ingredients: In another bowl, whisk pumpkin, oil, sugars, eggs, and vanilla until smooth.

Make batter: Gently fold dry ingredients into the wet mixture. Do not overmix.

Layer swirl: Pour half the batter into loaf pans. Sprinkle cinnamon-sugar mixture evenly. Top with remaining batter.

Swirl: Use a knife to gently swirl layers.

Bake: 25–30 minutes, or until a toothpick comes out clean.

Cool: Let loaves rest in the pan for 10 minutes, then transfer to a rack.

Cinnamon Swirl Pumpkin Bread Mini Loaves

Prep:15 minsCook:30 minsTotal:45 minsYield:4 mini loaves

Ingredients Loaf Batter

1 ¾ cups all-purpose flour

1 tsp baking soda

½ tsp baking powder

½ tsp salt

1 tsp ground cinnamon

½ tsp ground nutmeg

½ tsp ground ginger

½ tsp ground cloves

1 cup pumpkin purée

½ cup vegetable oil (or melted butter)

¾ cup granulated sugar

½ cup packed brown sugar

2 large eggs + 1 tsp vanilla

Cinnamon Swirl

½ cup brown sugar

1 tbsp ground cinnamon

Instructions

Preheat oven to 350°F (175°C). Grease 4 mini loaf pans or line with parchment.

Whisk flour, baking soda, baking powder, spices, and salt in a bowl.

In another bowl, whisk pumpkin, oil, sugars, eggs, and vanilla until smooth.

Fold dry ingredients into wet just until combined. Do not overmix.

Divide half the batter among pans. Sprinkle swirl mixture evenly. Top with remaining batter and gently swirl with a knife.

Bake 25–30 minutes, or until a toothpick comes out clean. Cool 10 minutes; transfer to a rack.

Tips: For add-ins, fold in ½ cup chocolate chips or chopped pecans.

For a crunchy top, finish with 1–2 tbsp cinnamon sugar before baking.

Loaves freeze well for up to 3 months.

Tips for the Best Pumpkin Bread Mini Loaves

Use fresh pumpkin purée for richer flavor.

Avoid overmixing the batter; it can make loaves dense.

For a crunchy topping, sprinkle cinnamon sugar on top before baking.

Mini loaves bake faster than a full loaf — check early!

Wrap cooled loaves in plastic to keep them moist.

Variations to Try

Chocolate Chip Pumpkin Loaves: Add ½ cup chocolate chips.

Glazed Loaves: Drizzle with cream cheese glaze.

Nutty Loaves: Stir in ½ cup chopped pecans or walnuts.

Spiced Loaves: Add extra ginger for warmth.

Vegan Version: Use flax eggs and coconut oil.

Storage and Freezing

Room temperature: Store in an airtight container up to 3 days.

Refrigerator: Keeps fresh up to 1 week.

Freezer: Wrap tightly and freeze for up to 3 months. Thaw overnight before serving.

FAQs

Q: Can I double this recipe? Yes, double it and bake 8 mini loaves or two large loaves.

Q: Can I make muffins instead? Absolutely! Divide into muffin tins and bake for 18–20 minutes.

Q: What’s the best topping? Cream cheese glaze or a cinnamon-sugar sprinkle works perfectly.

Final Thoughts

Cinnamon swirl pumpkin bread mini loaves are cozy, delicious, and versatile. They’re great for gifting, sharing, or enjoying with a warm drink. With a tender crumb and sweet swirl, these mini loaves are sure to become a seasonal favorite.

Creamy tortellini soup is one of the easiest and most comforting meals you can prepare in just 30 minutes. This recipe combines tender cheese-filled tortellini with a flavorful broth, aromatic vegetables, and a silky cream finish. It feels like a restaurant-quality soup but is simple enough for any busy weeknight dinner.

The best part is its flexibility. You can make it with Italian sausage for a heartier version, or keep it vegetarian with beans and extra greens. The rich broth balances creaminess with fresh spinach and Parmesan for a soup that satisfies without feeling heavy. It is also a one-pot recipe, which means minimal cleanup and a quick turnaround from stove to table.

In this guide, you will learn how to make creamy tortellini soup step by step. You will also discover variations, storage tips, and methods for making it in the slow cooker or Instant Pot.

Why You’ll Love This Creamy Tortellini Soup

Fast and easy: Ready in just 30 minutes, perfect for weeknights.

One-pot recipe: Everything cooks in a single pot, making cleanup simple.

Creamy but balanced: The broth keeps the soup light while cream adds richness.

Flexible: Works with Italian sausage, chicken, or vegetarian substitutions.

Family-friendly: Kids and adults love the cheesy tortellini and mild flavors.

Great leftovers: Easy to reheat for lunch or dinner the next day.

Ingredient Notes

Each ingredient in this creamy tortellini soup plays an important role. Below are the key components and why they matter:

Cheese tortellini: Refrigerated tortellini give the best texture, but frozen works with a few extra minutes of cooking.

Italian sausage (optional): Adds depth and savoriness. Sweet sausage gives a mild flavor, while hot sausage makes the soup spicier.

Aromatics: Onion, celery, and carrot form the classic Italian soffritto base, building sweetness and flavor.

Garlic & Italian seasoning: Essential herbs and spices for warmth and aroma.

Tomato paste: A small spoonful deepens color and brings umami.

Broth: Low-sodium chicken or vegetable broth gives you control over salt levels.

Heavy cream: Creates richness and body. Half-and-half can be used for a lighter texture.

Spinach or kale: Adds freshness and nutrients, balancing the creaminess.

Parmesan rind (optional): Simmering with a rind infuses deep umami flavor.

Lemon juice: Brightens the soup at the end, cutting through the richness.

Tip: This recipe makes about 6 servings (8 cups). Total cooking time is about 30 minutes.

Ingredients

Serves: 6Prep: 10 minCook: 20 min

Base

1 lb (450 g) Italian sausage, casing removed (optional)

2 tbsp olive oil (reduce if using sausage)

1 medium onion, finely diced

2 ribs celery, diced

2 medium carrots, diced

4 garlic cloves, minced

1 tbsp tomato paste

1 tsp Italian seasoning

1/2 tsp crushed red pepper flakes (optional)

Liquids & pasta

6 cups (1.4 L) low-sodium chicken or vegetable broth

1 parmesan rind (optional but excellent)

18–20 oz (500–560 g) refrigerated cheese tortellini

1 cup (240 ml) heavy cream

Greens & finish

4 cups baby spinach or 2 cups chopped kale

1 tbsp fresh lemon juice

1/3 cup finely grated Parmesan, plus more to serve

Kosher salt and black pepper, to taste

Substitutions: Use turkey sausage, rotisserie chicken, or white beans for protein. For a lighter soup, swap heavy cream with half-and-half plus 2 tsp cornstarch whisked into the broth.

Step-by-Step Instructions

Brown the sausage (if using): Heat a large pot over medium heat. Add the sausage and break it into small pieces. Cook until golden brown, about 5–6 minutes. Transfer to a plate, leaving about 1 tablespoon of fat in the pot. If skipping sausage, warm 2 tablespoons of olive oil instead.

Build the flavor base: Add onion, celery, and carrot to the pot. Season with a pinch of salt. Cook until the vegetables soften and become glossy, 6–8 minutes, stirring often.

Bloom aromatics: Stir in garlic, tomato paste, Italian seasoning, and red pepper flakes. Cook for 1–2 minutes until fragrant and the tomato paste darkens slightly.

Deglaze and simmer: Pour in the broth, scraping up any browned bits from the bottom. Drop in the Parmesan rind if using. Return sausage to the pot. Bring to a gentle boil, then reduce to a lively simmer. Cook for 8 minutes to meld the flavors.

Cook the tortellini: Add tortellini to the simmering broth. Cook gently until just tender—about 3–5 minutes for refrigerated tortellini or 6–7 minutes for frozen. Avoid overcooking as the pasta will continue to soften in hot broth.

Finish creamy: Reduce the heat to low. Stir in the heavy cream and spinach. Warm until the greens wilt, 1–2 minutes. Do not boil after adding cream to prevent curdling.

Balance and serve: Remove the Parmesan rind if used. Add lemon juice and grated Parmesan. Taste the soup and adjust with salt and black pepper as needed. Ladle into bowls and top with extra Parmesan and cracked pepper for serving.

Make-ahead tip: For best texture, cook tortellini separately if storing more than one day. Add freshly cooked pasta to the hot soup when serving.

Variations and Substitutions

Chicken & mushroom: Replace sausage with 2 cups sliced cremini mushrooms and add 2 cups shredded rotisserie chicken at the end of cooking.

Vegetarian: Skip sausage and add 1 can (15 oz) of cannellini beans, drained and rinsed. Use vegetable broth instead of chicken broth.

Tomato-cream (rosa) version: Stir in one 14-oz can of crushed tomatoes along with the broth for a blush-colored, tangy variation.

Tuscan-style: Use chopped lacinato kale instead of spinach and add 1/3 cup chopped sun-dried tomatoes for an earthy, rustic flavor.

Spicy kick: Use hot Italian sausage and double the red pepper flakes if you like heat.

Herb upgrade: Stir in fresh basil and parsley just before serving. Add 1 teaspoon fresh thyme with the aromatics for a woodsy note.

Cheese variation: Try spinach-ricotta or three-cheese tortellini for a different flavor profile.

Gluten-free option: If available, use gluten-free tortellini. Otherwise, substitute gluten-free gnocchi and reduce cooking time slightly.

Make It Dairy-Free or Lighter

Dairy-free: Replace heavy cream with 3/4 cup unsweetened oat creamer or cashew cream. Skip Parmesan or use a dairy-free alternative.

Lighter version: Use 1/2 cup half-and-half combined with 1/2 cup evaporated milk. For body, whisk 2 teaspoons cornstarch into the broth before adding the dairy.

Lower sodium: Choose low-sodium broth and adjust salt at the end. Keep in mind Parmesan is naturally salty, so taste before adding more.

Slow Cooker Directions

Brown the sausage (optional but recommended): In a skillet, cook sausage until golden, then transfer to the slow cooker.

Add vegetables and seasonings: Stir in onion, celery, carrot, garlic, tomato paste, Italian seasoning, red pepper flakes, and broth.

Cook the base: Cover and cook on LOW for 6–7 hours or HIGH for 3–4 hours.

Add tortellini: Turn the slow cooker to HIGH and stir in the tortellini. Cook for 15–25 minutes until just al dente. Check after 12 minutes to prevent mushy pasta.

Finish creamy: Stir in the cream and spinach. Warm through for 5 minutes. Add lemon juice and Parmesan before serving.

Tip: Every slow cooker is different. Always taste and test pasta for doneness a little earlier to avoid overcooking.

Instant Pot Directions

Sauté the base: Select Sauté and brown sausage in 1 tablespoon oil. Add onion, celery, and carrot. Cook for 3 minutes, stirring often. Stir in garlic, tomato paste, and Italian seasoning for 30 seconds until fragrant.

Deglaze: Pour in broth, scraping the bottom to prevent the “Burn” warning. Add the Parmesan rind if using.

Pressure cook: Seal the lid. Cook on High Pressure for 1 minute. Quick release the steam once the timer ends.

Add tortellini: Switch back to Sauté (Low). Stir in the tortellini and simmer gently for 3–5 minutes until al dente.

Finish: Stir in the cream and spinach. Heat gently without boiling. Add lemon juice and Parmesan. Taste and season with salt and pepper before serving.

What to Serve With Creamy Tortellini Soup

Garlic bread: Perfect for soaking up the creamy broth.

Simple green salad: A crisp salad with lemon vinaigrette balances the richness.

Roasted vegetables: Try broccoli, Brussels sprouts, or zucchini for extra nutrition.

Antipasto plate: Offer olives, cured meats, and marinated peppers as a starter.

Beverage pairing: A glass of Pinot Grigio or sparkling water with lemon complements the flavors.

Storage, Freezing, and Reheating

Refrigerator: Store the soup without tortellini for up to 4 days. Keep pasta in a separate container to avoid sogginess.

Freezer: Freeze the broth and vegetables without pasta or cream for up to 3 months. Add tortellini and dairy only after reheating.

Reheating: Warm gently on the stove over medium-low heat. Avoid boiling after cream is added. Add a splash of broth if the soup thickens too much.

Tip: For best texture, always cook tortellini fresh and add it to reheated soup just before serving.

Nutrition Snapshot

Approximate values per serving (1/6 of recipe, made with sausage and heavy cream). Actual values vary by brands and substitutions.

Calories~510

Protein~21 g

Carbohydrates~46 g

Fat~27 g

Fiber~3 g

Sugars~6 g

Sodium*varies

*Sodium depends heavily on broth, cheese, and tortellini brands. Use low-sodium broth and season to taste.

Troubleshooting & Pro Tips

Avoid mushy tortellini: Cook just until al dente. Remember, pasta continues cooking in hot broth.

Prevent curdling: Lower the heat before adding cream and never let it boil after dairy goes in.

Balance richness: A squeeze of lemon juice or a splash of vinegar brightens heavy cream.

Layer seasoning: Add a pinch of salt to vegetables early, then adjust at the end after adding Parmesan.

Boost flavor: Parmesan rinds simmered in broth add deep umami — keep them in your freezer for soups.

Make-ahead strategy: Cook the broth base first. Add tortellini and cream only when reheating to serve.

With these small adjustments, your creamy tortellini soup will turn out perfect every time.

Frequently Asked Questions

Can I use frozen tortellini?

Yes, frozen tortellini works fine. Add directly to the simmering broth and cook 2–3 minutes longer than refrigerated tortellini. Start tasting early to keep it al dente.

How do I stop the cream from curdling?

Lower the heat before adding cream and keep the soup below a boil. If using half-and-half, whisk 1–2 teaspoons cornstarch into it first to stabilize.

What protein can I use instead of sausage?

Shredded rotisserie chicken, leftover turkey, or a can of rinsed cannellini beans all work well. Add them at the end to avoid overcooking.

Can I make this soup ahead of time?

Yes. Prepare the broth and vegetables ahead and refrigerate. Add tortellini and cream only when reheating to keep the texture fresh.

Is there a gluten-free option?

Yes, use gluten-free tortellini if available. Alternatively, swap in gluten-free gnocchi and reduce the cooking time slightly.

Still have questions? Leave a comment below and I’ll be happy to help.

Craving bold takeout flavor at home? This Black Pepper Chicken recipe brings you the irresistible punch of freshly ground black pepper, savory sauce, and tender chicken—all in under 30 minutes. Popular in Asian-inspired kitchens, this dish is known for its rich, aromatic flavor and quick cooking time.

Instead of ordering takeout, you can recreate this restaurant classic with simple pantry ingredients. The combination of seared chicken, a glossy pepper sauce, and stir-fried veggies makes it perfect for busy weeknights or meal prep.

Whether you’re a spice lover or simply seeking a new go-to chicken dinner, this homemade black pepper chicken delivers a flavorful, healthier alternative that satisfies every time.

What Is Black Pepper Chicken?

Black Pepper Chicken is a flavorful stir-fry dish commonly found in Chinese-American cuisine. It’s made with tender chicken pieces sautéed with vibrant vegetables and coated in a bold black pepper sauce.

Unlike sweet or sticky Asian dishes, this one leans into savory and spicy flavors. The star ingredient—coarsely ground black pepper—gives the dish its signature kick, while soy sauce, garlic, and onions provide balance and umami depth.

Traditionally served over steamed rice or noodles, black pepper chicken is a fast, satisfying meal perfect for busy households. It’s especially loved for its combination of quick prep time, high protein, and bold flavor, making it a healthier alternative to deep-fried takeout options.

Ingredients You’ll Need for Black Pepper Chicken

To make Black Pepper Chicken at home, you’ll need simple ingredients commonly found in most kitchens. Here’s a breakdown of the essentials:

For the Chicken:

1 lb (450g) boneless, skinless chicken thighs or breasts, cut into bite-sized pieces

1 tablespoon cornstarch (for coating and tenderness)

1 tablespoon soy sauce

1 tablespoon vegetable oil (or sesame oil for extra flavor)

For the Stir-Fry Vegetables:

1 green bell pepper, sliced

1 red bell pepper, sliced

1 small onion, sliced

2 cloves garlic, minced

1-inch piece of fresh ginger, grated or finely chopped

For the Sauce:

2 tablespoons soy sauce (low-sodium preferred)

1 tablespoon oyster sauce (adds richness and umami)

1 teaspoon dark soy sauce (for color, optional)

1–1.5 teaspoons freshly ground black pepper (adjust to heat preference)

1/2 teaspoon sugar

1/4 cup chicken broth or water

1 teaspoon cornstarch mixed with 1 tablespoon water (slurry to thicken the sauce)

📝 Tip: Freshly cracked black pepper makes a big difference. Use a coarse grind for that bold, spicy kick.

How to Make Black Pepper Chicken (Step-by-Step)

Follow these simple steps to prepare flavorful and authentic Black Pepper Chicken at home:

1. Marinate the Chicken

In a bowl, combine the chicken pieces with soy sauce and cornstarch. Mix well until the chicken is evenly coated. Let it marinate for at least 15 minutes. This step ensures the chicken remains tender and absorbs flavor.

2. Prepare the Sauce

In a small bowl, whisk together soy sauce, oyster sauce, dark soy sauce (if using), black pepper, sugar, chicken broth, and the cornstarch slurry. Set this aside for later.

3. Cook the Chicken

Heat 1 tablespoon of oil in a large skillet or wok over medium-high heat. Add the marinated chicken in a single layer. Sear and cook until golden brown and cooked through, about 4–5 minutes. Remove from the skillet and set aside.

4. Stir-Fry the Vegetables

In the same pan, add a bit more oil if needed. Sauté the garlic and ginger for 30 seconds until fragrant. Add sliced onions and bell peppers. Stir-fry for 2–3 minutes until they are slightly tender but still crisp.

5. Combine Everything

Return the cooked chicken to the pan. Pour the sauce mixture over the chicken and vegetables. Toss everything together and cook for 2–3 minutes, allowing the sauce to thicken and coat the chicken evenly.

6. Serve

Turn off the heat. Serve hot over steamed white rice or noodles. Garnish with additional freshly ground black pepper if desired.

Why You’ll Love This Black Pepper Chicken Recipe

This Black Pepper Chicken is more than just a quick dinner idea—it’s a recipe you’ll want to make again and again. Here’s why:

1. Bold, Savory Flavor

The rich black pepper sauce delivers a deep, savory heat that wakes up your taste buds. The combination of soy sauce, oyster sauce, and fresh cracked pepper creates a layered flavor that’s both comforting and exciting.

2. Quick and Easy to Make

With just a few pantry staples and about 30 minutes of cooking time, this dish comes together fast. It’s ideal for busy weeknights when you need something fast but delicious.

3. Budget-Friendly

Chicken thighs or breasts are affordable, and the vegetables are flexible. You can easily swap ingredients based on what you already have—perfect for cutting costs without sacrificing flavor.

4. Healthier Than Takeout

Homemade Black Pepper Chicken uses fewer oils and no artificial additives. You’re in control of the ingredients, which means you can enjoy your meal with fewer calories and less sodium.

5. Versatile and Customizable

You can tailor this recipe to your liking. Prefer it spicier? Add chili flakes. Need it gluten-free? Use tamari instead of soy sauce. Want more veggies? Toss in snap peas or broccoli.

Tips for Perfect Black Pepper Chicken Every Time

Mastering Black Pepper Chicken is easy, but a few smart tips will make your dish restaurant-quality:

1. Use Freshly Cracked Black Pepper

Avoid pre-ground pepper. Freshly cracked black pepper gives the sauce its signature kick and aroma. It balances perfectly with the soy and oyster sauces.

2. Marinate the Chicken

Marinating the chicken for at least 15–20 minutes in soy sauce and cornstarch makes it more flavorful and tender. It also helps seal in juices during cooking.

3. High Heat Is Key

Cook over high heat to sear the chicken properly and lock in flavor. This technique helps achieve that characteristic wok-charred taste similar to your favorite takeout.

4. Cut the Chicken Evenly

Cut the chicken into bite-sized, uniform pieces. This ensures even cooking and makes every bite delicious and easy to eat.

5. Don’t Overcook the Vegetables

Add bell peppers and onions toward the end to keep them crisp. Overcooked vegetables will make the dish soggy and dull.

6. Use a Wok or Large Skillet

A wok distributes heat more evenly and gives you enough room to toss the ingredients quickly. If you don’t have one, use the largest skillet you own.

How to Make Black Pepper Chicken: Step-by-Step Instructions

Follow these simple steps to prepare delicious and flavorful Black Pepper Chicken at home.

Ingredients

Here’s everything you need:

For the Chicken:

1 lb (450g) boneless, skinless chicken thighs or breasts, cut into bite-sized pieces

1 tbsp soy sauce

1 tbsp cornstarch

1 tbsp oil (vegetable or sesame)

For the Sauce:

2 tbsp oyster sauce

1 tbsp dark soy sauce

1 tbsp light soy sauce

1 tsp sugar

2 tsp freshly ground black pepper

1 tsp rice vinegar or apple cider vinegar

1 tbsp water (to thin the sauce if needed)

Vegetables:

1 green bell pepper, sliced

1 red bell pepper, sliced

1 small onion, sliced

2–3 garlic cloves, minced

1-inch piece of ginger, grated

Instructions

Step 1: Marinate the Chicken In a medium bowl, mix the chicken pieces with soy sauce and cornstarch. Set aside for 15–20 minutes to marinate.

Step 2: Prepare the Sauce In a small bowl, whisk together oyster sauce, light soy sauce, dark soy sauce, sugar, vinegar, and black pepper. Set aside.

Step 3: Cook the Chicken Heat 1 tablespoon of oil in a wok or large skillet over medium-high heat. Add the marinated chicken and stir-fry until golden brown and fully cooked. Remove the chicken and set it aside.

Step 4: Sauté the Aromatics In the same pan, add a little more oil if needed. Add garlic and ginger, and stir-fry for 30 seconds until fragrant.

Step 5: Add Vegetables Add bell peppers and onions. Stir-fry for 2–3 minutes. Keep them slightly crisp.

Step 6: Combine Everything Return the cooked chicken to the pan. Pour in the prepared sauce. Stir everything together and cook for another 1–2 minutes until the sauce thickens and coats the chicken evenly.

Step 7: Serve Serve hot with steamed rice or noodles. Garnish with sliced green onions if desired.

Serving Suggestions and Flavorful Variations

Black Pepper Chicken is incredibly versatile and pairs well with many sides. Whether you’re serving it for lunch or dinner, these suggestions and variations will elevate your meal.

Serving Suggestions

With Steamed Rice: Classic and comforting. White jasmine rice or brown rice balances the bold flavors of the dish.

With Fried Rice: Combine with egg fried rice or vegetable fried rice for a full takeout-style meal.

With Noodles: Serve over lo mein, rice noodles, or soba for a flavorful fusion twist.

In Lettuce Wraps: Spoon the chicken into crisp lettuce leaves for a low-carb, fresh serving option.

Alongside Steamed Veggies: Broccoli, snap peas, or bok choy add extra nutrients and crunch.

Delicious Variations

Add Cashews or Peanuts: Stir in roasted nuts at the end for extra crunch and a nutty undertone.

Make it Spicier: Add sliced red chilies or a dash of chili oil to the sauce for extra heat.

Use Tofu or Mushrooms: Replace the chicken with crispy tofu or stir-fried mushrooms for a vegetarian version.

Try Different Proteins: Swap chicken for shrimp, beef strips, or pork for variety.

Add a Citrus Twist: A splash of lime juice or grated orange zest can brighten the overall flavor profile.

Storage and Reheating Tips

Proper storage and reheating ensure your Black Pepper Chicken remains just as flavorful the next day. Here’s how to keep it fresh and safe:

How to Store Leftovers

Refrigerator: Place cooled chicken in an airtight container. Store for up to 3–4 days in the fridge.

Freezer: For longer storage, freeze in a sealed freezer-safe container for up to 2 months. Tip: Freeze in portions to make reheating easier.

How to Reheat

On the Stovetop: Reheat in a skillet over medium heat with a splash of water or chicken broth. Stir occasionally until warmed through.

In the Microwave: Place in a microwave-safe dish, cover lightly, and heat in 30-second intervals, stirring between each, until hot.

From Frozen: Thaw overnight in the fridge, then reheat using one of the methods above.

Frequently Asked Questions (FAQs)

1. Can I make Black Pepper Chicken less spicy?

Yes, you can. Simply reduce the amount of freshly ground black pepper. You can also use sweet bell peppers and a milder chili sauce if your recipe includes one.

2. What is the best cut of chicken for this recipe?

Boneless, skinless chicken thighs are the most flavorful and tender. However, chicken breasts work well too if you prefer leaner meat.

3. Can I make this dish ahead of time?

Absolutely. You can prepare the sauce and chop the vegetables ahead. Cooked Black Pepper Chicken also reheats well, making it perfect for meal prep.

4. Is this recipe gluten-free?

It can be if you use gluten-free soy sauce or tamari. Always check the labels of all sauces and condiments used.

5. What vegetables go well with Black Pepper Chicken?

Bell peppers, onions, broccoli, snap peas, and carrots all complement the dish beautifully. Feel free to add your favorites.

6. How can I make the sauce thicker?

Mix a little cornstarch with cold water (a slurry) and add it at the end of cooking. Stir continuously until the sauce thickens.

Final Thoughts on Black Pepper Chicken

Black Pepper Chicken is more than just a quick meal—it’s a savory dish bursting with bold flavor and comforting spice. With its flexible ingredients and simple preparation, it fits perfectly into any weeknight dinner routine or even special occasions.

Whether you’re cooking for family or impressing guests, this recipe delivers satisfaction in every bite. Plus, it’s easy to customize based on your spice tolerance and pantry staples.

Ready to spice up your dinner tonight? Give this Black Pepper Chicken recipe a try and discover why it’s a favorite across cultures and kitchens. And if you loved it, don’t forget to share it, bookmark the recipe, and explore more chicken dishes on our blog.

Budgeting isn’t about restriction—it’s about control, freedom, and financial security. In this guide, you’ll learn: ✅ Why most budgets fail (and how to avoid those mistakes) ✅ Step-by-step instructions to build a budget that works ✅ Proven budgeting methods (pick the best one for your lifestyle) ✅ Tips to stick to your budget (without feeling deprived)

Do you feel like your money disappears before the month ends? Are you tired of living paycheck to paycheck? If so, you’re not alone—many people struggle with managing their finances. The good news? A well-structured budget can change everything.

✅ Fix: Create a “sinking fund” for unexpected or annual expenses.

4. No Emergency Fund

Without savings, emergencies force debt.

✅ Fix: Save $1,000 ASAP, then build 3-6 months’ expenses.

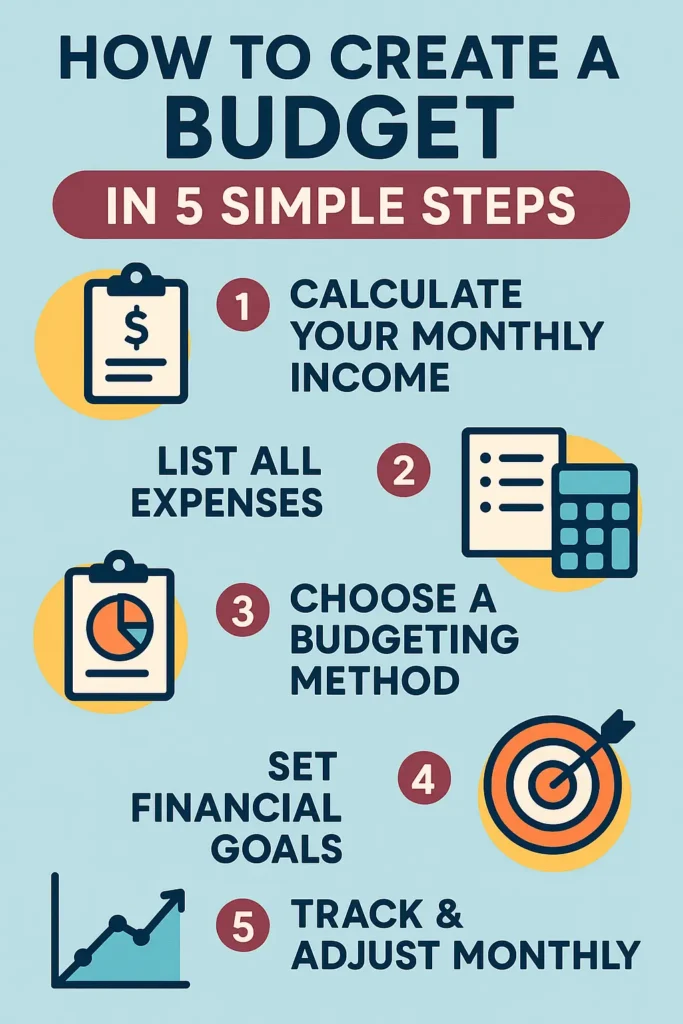

Section 2: How to Create a Budget in 5 Simple Steps

Step 1: Calculate Your Monthly Income

Begin by determining your total monthly income, which includes all sources such as your salary, bonuses, freelance work, and any passive income streams. This foundational step is crucial as it sets the stage for understanding how much money you have available to allocate towards expenses and savings.

Include:

Salary (after taxes)

Side hustles

Passive income

❌ Mistake: Budgeting with gross (pre-tax) income.

Step 2: List All Expenses

Next, compile a comprehensive list of all your expenses. Categorize them into fixed expenses, like rent or mortgage payments, and variable expenses, such as groceries and entertainment. This detailed overview will help you understand where your money is going each month.

Fixed Expenses:

Rent/mortgage

Utilities

Insurance

Variable Expenses:

Groceries

Entertainment

Dining out

Irregular Expenses:

Car maintenance

Gifts

Subscriptions

✅ Pro Tip: Review 3 months of bank statements to catch hidden spending.

Step 3: Choose a Budgeting Method

After identifying your income and expenses, select a budgeting method that suits your lifestyle. Popular approaches include the envelope system, zero-based budgeting, or the 50/30/20 rule. Each method has its own advantages, so choose one that aligns with your financial goals and habits.

Pick one that fits your lifestyle:

A. 50/30/20 Budget

50% Needs (rent, bills, groceries)

30% Wants (dining, hobbies)

20% Savings/Debt

✅ Best for: Beginners who want flexibility.

B. Zero-Based Budget

Every dollar has a job (even savings).

Example: If you earn 3,000∗∗,allocateall∗∗3,000∗∗,allocateall∗∗3,000.

✅ Best for: Detail-oriented planners.

C. Cash Envelope System

Use cash only for categories like groceries and entertainment.

✅ Best for: Overspenders (forces discipline).

Step 4: Set Financial Goals

Establish clear financial goals to guide your budgeting process. Whether you aim to save for a vacation, pay off debt, or build an emergency fund, having specific targets will motivate you to stick to your budget and make informed spending decisions.

Examples:

Short-term: Save $500 emergency fund

Mid-term: Pay off $2,000 credit card debt

Long-term: Save for a house down payment

✅ Pro Tip: Use SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound).

Step 5: Track & Adjust Monthly

Finally, make it a habit to track your spending and adjust your budget monthly. Regularly reviewing your financial situation allows you to identify areas for improvement and adapt to any changes in income or expenses, ensuring that your budget remains effective and relevant.

Weekly check-ins (avoid surprises)

Monthly reviews (adjust categories as needed)

✅ Tool Recommendation:YNAB (You Need a Budget) helps with real-time adjustments.

Section 3: How to Stick to Your Budget (Without Going Crazy)

1. Automate Savings & Bills

Set up auto-transfers to savings.

Use auto-pay for bills to avoid late fees.

2. Use the “24-Hour Rule” for Non-Essential Purchases

Wait 24 hours before buying—avoid impulse spending.

3. Reward Yourself (Responsibly)

Example: If you stay under budget for 3 months, treat yourself to a small splurge.

4. Try a No-Spend Challenge

7-day no-spend challenge (only essentials).

Helps reset spending habits.

5. Find an Accountability Partner

Share goals with a friend or spouse—motivation boosts success.

Section 4: Advanced Budgeting Tips

1. Negotiate Bills

Call providers (internet, insurance) to lower rates.

Budgeting isn’t about deprivation—it’s about making your money work for you. By following these steps, you’ll: ✔ Stop living paycheck to paycheck ✔ Build savings & crush debt ✔ Gain peace of mind

Action Step: Start today—open a spreadsheet or budgeting app and track your last month’s spending. Small steps lead to big wins!

It is not simple to save for kids college without sacrificing retirement. Many parents face the challenge of finding a balance between saving for their children’s college education and ensuring their own retirement. It is essential to develop a strategic approach that allows you to contribute to both goals without compromising your financial future. But is it really possible?

Yes, with the right financial planning, you can help your kids avoid student debt while securing your own retirement. This guide offers step-by-step strategies to reach both goals without compromise.

Why Parents Struggle to Balance College and Retirement Savings

To save for kids college without sacrificing retirement, finding an optimal balance with these goals is more convenient. Parents often find themselves in a challenging position when it comes to managing their financial priorities, particularly when it involves the dual responsibilities of funding their children’s college education and securing their own retirement savings.

The pressure to provide for their children’s future can lead to difficult decisions. Many parents feel compelled to invest heavily in college funds, often at the expense of their long-term financial security. Rising tuition costs and the increasing burden of student debt exacerbate this struggle, creating a sense of urgency to save for education.

Simultaneously, the reality of retirement looms, with many parents aware that neglecting their savings could jeopardize their financial stability later. Balancing these two significant financial goals requires careful planning and prioritization. Yet, the emotional weight of wanting to support their children can cloud judgment, making it even more challenging to strike the right balance.

Step 1: Set Clear Priorities

Begin by identifying what matters most to you. Ensure that your retirement and your children’s education are given appropriate weight in your financial planning.

Priority

Timeline

Importance

Retirement

20–30 years

Essential

Kids’ College

10–18 years

Very Important

While both are critical, retirement lacks borrowing options. Your child can get scholarships, grants, or loans, but you can’t take a loan for retirement.

Assess the total amount you need for your child’s college education, including tuition, fees, and living expenses, to create a comprehensive savings target.

🔹 Estimate Retirement Needs

Use a retirement calculator. Most people need 70–80% of their pre-retirement income annually.

Once you have both targets, you can set monthly savings goals.

Planning for two major financial goals requires a broader perspective. Check out Mastering Finances for Families to get a holistic view of managing your household’s money more effectively.

Step 3: Maximize Retirement Contributions First

Focus on maximizing your retirement savings first, as this will secure your financial future and provide a stable foundation before allocating funds for college. Before contributing to college savings, prioritize these:

401(k) or 403(b): Get the full employer match—it’s free money

Traditional or Roth IRA: Tax-advantaged growth for retirement

Health Savings Account (HSA): If eligible, offers triple tax advantages

Building retirement early allows compounding to work in your favor.

Want to know how much you can safely withdraw later in life? Learn more about the Four Percent Rule, a key retirement strategy.

Step 4: Choose the Right College Savings Account

After securing retirement contributions, explore these college savings options:

✅ 529 College Savings Plan

Tax-free growth and withdrawals for education

High contribution limits

May qualify for state tax deductions

Some plans allow you to change the beneficiary, so leftover funds can be used for another child or even your own continuing education.

✅ Coverdell ESA

Tax-free for qualified expenses

Annual contribution cap: $2,000 per child

Income limits apply

✅ Custodial Accounts (UGMA/UTMA)

No restriction on how funds are used

Could impact financial aid eligibility

Less tax-advantaged

Step 5: Encourage Your Child to Contribute

Encourage your child to contribute a portion of their earnings from part-time jobs or allowances to education funding, fostering a sense of responsibility. Saving for college should be a shared responsibility.

Encourage your child to apply for scholarships and grants

Suggest they work part-time or during the summer

Involve them in the budgeting process

Teach them financial literacy early

This builds ownership and reduces your financial burden.

Step 6: Balance Your Monthly Budget

Review your monthly expenses and income to ensure you can allocate retirement and college savings funds without compromising your financial stability. Use a zero-based budget to allocate every dollar.

Fund retirement accounts

Pay essential living expenses

Allocate monthly savings for college

Avoid unnecessary expenses

Look for small cuts in lifestyle inflation. Instead of skipping retirement contributions, reduce discretionary spending like travel, subscriptions, or dining out.

Step 7: Use Windfalls and Bonuses Wisely

When you receive bonuses, tax refunds, or other unexpected financial windfalls, consider directing some funds towards your college savings to boost your progress. Any extra income should support your top financial priorities.

Tax refunds

Work bonuses

Inheritance or gifts

Split these between retirement and college savings. For instance, 70% of the budget should be allocated to retirement, and 30% to college.

Step 8: Avoid These Common Mistakes

Steer Clear of Common Pitfalls: Educate yourself about frequent mistakes in saving for college, such as underestimating costs or neglecting to take advantage of available financial aid options.

Mistake

Why It’s Harmful

Prioritizing college over retirement

You risk being dependent in old age

Stopping retirement contributions

You lose compound growth

Using home equity loans

Adds risk if housing values drop

Co-signing large student loans

You become legally responsible if your child defaults

Step 9: Explore Other Ways to Pay for College

Investigate Alternative Funding Sources: Look into scholarships, grants, and work-study programs that can help alleviate the financial burden of college expenses, providing additional support beyond your savings. Not all the burden should fall on your savings. Consider:

Financial aid: Complete the FAFSA early

Community college: Start with lower-cost education

Employer tuition assistance: Some jobs offer educational benefits

Student loans (with caution): As a last resort

Step 10: Reassess Your Plan Annually

Review and Adjust Your Strategy Annually: Regularly evaluate your savings plan to ensure it remains aligned with your financial goals and make necessary adjustments based on changes in income, expenses, or educational costs.

Have your income or expenses changed?

Are investment returns aligned with expectations?

Is your child choosing a more or less expensive college?

Getting a handle on how to build credit from scratch is an essential financial skill that everyone should learn. Whether you’re a young adult just starting out, a recent immigrant finding your way, or someone embarking on a fresh chapter in life, establishing a strong credit profile can open doors to better loan options, housing opportunities, and even job prospects. This guide will walk you through the steps to create credit from the ground up, even if you don’t have any credit history at the moment.

Why Learning How to Build Credit From Scratch Matters

Before moving to the steps, let’s cover why building credit from scratch is necessary. Understanding the importance of building credit is essential because it creates a world of benefits. When you establish a solid credit history, you can enjoy lower interest rates on loans and credit cards, making it easier on your wallet when you need to borrow. Plus, having good credit can significantly improve your chances of getting approved for rentals and mortgages, as landlords and lenders often look at your creditworthiness.

On top of that, a strong credit profile can lead to better job opportunities, especially in the finance industry, where trust is key. As you work on building a positive credit history, you might also find yourself eligible for higher credit limits, which shows lenders that they can count on you to handle your finances responsibly. Ultimately, your credit score is a vital sign of your reliability, demonstrating your ability to manage money wisely and helping you secure loans with more favorable terms.

In summary, Build Credit effectively helps to:

✅ Approval for Loans/Apartments – Landlords and lenders check credit first ✅ Save Thousands on Interest – Good credit = lower rates on mortgages/car loans ✅ Financial Security – Emergencies become easier to handle with credit access

A strong credit score helps you avoid common money mistakes in your 20s by giving you access to better financial tools and lower interest rates early in life.

Step 1: Understand the Basics of Credit

Before building credit, understand these essential terms:

Term

Meaning

Credit Score

A number (300–850) indicating your creditworthiness

Credit Report

A detailed history of your credit activities

FICO Score

The most common credit scoring model

Credit Bureau

Agencies (Equifax, Experian, TransUnion) that report your credit data

What Affects Your Credit Score:

Factor

Weight

Payment History

35%

Amounts Owed

30%

Length of Credit History

15%

New Credit

10%

Credit Mix

10%

Step 2: Review Your Current Credit History

Many beginners assume they’re starting from zero when learning how to build credit from scratch, but you might have hidden history from:

Student loans

Being an authorized user

Utility bills (in some cases)

How to check:

Use AnnualCreditReport.com (free weekly reports until 2023)

Sign up for Credit Karma (free VantageScore)

Step 3: Open a Secured Credit Card

A secured credit card is one of the easiest ways to build credit from scratch.

Requires a refundable deposit (usually $200–$500)

The deposit becomes your credit limit

You must use it responsibly and pay the full balance each month

Tip: Choose a card that reports to all three credit bureaus. You may qualify for an unsecured credit card after 6–12 months of on-time payments.

Step 4: Become an Authorized User

Ask a parent, relative, or trusted friend to add you as an authorized user on their existing credit card.

Their credit history will be added to your report

You don’t need to use the card

You benefit from their responsible credit habits

Note: Ensure the primary cardholder has good credit and low utilization.

Step 5: Apply for a Credit-Builder Loan

A credit-builder loan is specifically designed to help people build credit.

You borrow a small amount (e.g., $500–$1000)

The bank holds the money in a savings account

You make fixed monthly payments

At the end, you receive the money and a positive credit history

For more on how these loans work, read What Is a Personal Loan? to explore different types of personal loans and how to apply.

Look for credit-builder loans from credit unions or community banks. Credit-builder loans work similarly to small personal loans. If you’re considering one, check out our guide to personal loan rates to understand how interest rates vary across lenders.

Step 6: Use a Co-Signer

If you’re having trouble qualifying for a loan or credit card, a co-signer with good credit can help.

They guarantee the loan or credit card

You build credit through regular, on-time payments

If you default, the co-signer is responsible

Use this option carefully and only with mutual trust.

Step 7: Make On-Time Payments – Always

Payment history is the most important factor in your credit score.

Pay all credit card bills and loan installments on or before the due date

Set up automatic payments or calendar reminders

Even one late payment can drop your score significantly.

Step 8: Keep Credit Utilization Low

Your credit utilization ratio is the percentage of available credit you’re using.

Aim to use less than 30% of your limit

For example, if your limit is $500, keep your balance under $150

Lower utilization = higher score

Step 9: Don’t Apply for Too Much Credit at Once

Each credit application triggers a hard inquiry, which slightly lowers your score.

Limit credit card or loan applications

Only apply for what you genuinely need

Too many inquiries signal risk to lenders

Step 10: Be Patient and Stay Consistent

Credit building takes time. There are no shortcuts.

Continue using your secured card or credit-builder loan

Pay all bills on time

Avoid maxing out your card

After 6–12 months, your credit score will start to reflect your responsible habits

Step 11: Monitor and Improve

Track your credit-building progress with:

Experian’s free dashboard

CreditWise from Capital One

NerdWallet’s score simulator

Step 12: Grow Your Credit Profile

After 6 months of building credit from scratch, add:

A second credit card

A small installment loan

Rent reporting via services like RentTrack

Warning: Space applications 6+ months apart to avoid hard inquiry damage.

Common Mistakes to Avoid

Mistake

Why It Hurts

Missing payments

Lowers score, adds late fees

Maxing out cards

Increases credit utilization

Closing old accounts

Shortens credit history

Applying too often

Results in multiple hard inquiries

Ignoring your credit report

Errors go unnoticed and uncorrected

Final Thoughts: You Now Know How to Build Credit From Scratch

By following this step-by-step guide to build credit from scratch, you’ll go from no credit to good credit (670+) within 12-24 months. Remember:

Start with secured cards or credit-builder loans

Always pay on time

Grow your profile slowly and steadily

Need help managing money while building credit? Pair this guide with our Ultimate Budgeting Blueprint for complete financial success!

FAQs About Building Credit from Scratch

How long does it take to build credit from scratch?

Usually 3 to 6 months to generate a score, but longer to reach a good score (700+).

Can I build credit without a credit card?

Yes. Use credit-builder loans, report rent/utility payments, or become an authorized user.

Does paying rent help build credit?

Only if your rent payments are reported to credit bureaus through services like RentTrack or Experian Boost.

What credit score do I start with?

You don’t start with a score. It begins generating once you have credit activity for 3–6 months.

Managing money in your 20s can be challenging, but avoiding common financial pitfalls sets the foundation for long-term success. Many young adults make money mistakes in your 20s that lead to debt, poor credit, or missed investment opportunities. By recognizing these errors early, you can build wealth, secure your future, and achieve financial freedom.

In this comprehensive guide, we’ll explore the 10 money mistakes in your 20s and provide detailed, actionable tips on how to avoid them. We’ll cover everything from emergency funds to retirement planning, giving you the tools you need to make smart financial decisions that will benefit you for decades to come.

1. Not Building an Emergency Fund

One of the biggest money mistakes in your 20s is failing to save for emergencies. Without a financial safety net, unexpected expenses like medical bills, car repairs, or sudden job loss can force you into debt that takes years to repay.

Why It’s a Problem:

40% of Americans can’t cover a $400 emergency expense

Without savings, you may rely on high-interest credit cards

Financial stress can impact mental health and decision-making

How to Avoid This Mistake:

Determine your target amount: Aim for 3-6 months of living expenses

Start small: Even $50 per month adds up over time

Automate savings: Set up automatic transfers to a dedicated account

Choose the right account: Use a high-yield savings account (HYSA) to earn interest while keeping funds accessible

Rebuild after use: If you dip into your emergency fund, prioritize replenishing it

Real-World Example:

Sarah, a 24-year-old graphic designer, avoided financial disaster when her car needed 1,200inrepairsbecauseshehadbuilta1,200inrepairsbecauseshehadbuilta5,000 emergency fund over two years. Without it, she would have had to put the repairs on a credit card with 22% interest.

2. Money mistakes in your 20s: Living Beyond Your Means

Overspending on luxuries like dining out, expensive gadgets, or premium apartments is a common money mistake in your 20s that leads to financial stress and prevents wealth building.

Why It’s a Problem:

Lifestyle inflation keeps you from saving

Can lead to credit card debt

Delays in important financial milestones

How to Avoid such money mistakes in your 20s

Follow the 50/30/20 rule:

50% on needs (rent, groceries, utilities)

30% on wants (entertainment, dining out)

20% on savings/debt repayment

Track spending: Use apps like Mint or YNAB

Wait 24 hours before big purchases

Find affordable alternatives:

Cook at home instead of daily takeout

Use public transportation instead of expensive car payments

Set spending limits for discretionary categories

Case Study:

Mike, a 26-year-old engineer, was spending $800/month on food delivery and entertainment. He cut this to $300/month by meal prepping and finding free activities, freeing up $6,000 annually for investments.

Sticking to a budget is crucial—learn how to create one for every life stage in our complete budgeting guide.

3. Ignoring Your Credit Score

Your credit score affects loans, rentals, insurance rates, and job opportunities. Neglecting it is a major money mistake in your 20s with long-term consequences.

Why It Matters:

Good credit (700+) saves thousands in interest

Landlords often require 650+ scores

Some employers check credit for certain positions

How to Build Good Credit:

Pay all bills on time (set up autopay)

Keep credit utilization below 30% (ideally under 10%)

Don’t close old accounts (lengthens credit history)

Limit hard inquiries (space out credit applications)

Credit Score Breakdown:

35% Payment history

30% Amounts owed

15% Length of credit history

10% New credit

10% Credit mix

4. Not Investing Early

Waiting to invest is one of the most costly money mistakes in your 20s due to the power of compound interest. Even small, regular investments can grow significantly over decades.

The Power of Starting Early:

200/monthat7200/monthat7402,000 in 40 years

Waiting 10 years to start could cost you $200,000+ in potential growth

Tax-advantaged accounts multiply your returns

How to Start Investing:

Maximize employer retirement matches (free money)

Open a Roth IRA (tax-free growth)

Invest in low-cost index funds (VTI, VOO)

Automate contributions (set it and forget it)

Increase contributions with raises

Investment Comparison:

Age Started

Monthly Investment

Total by Age 65 (7% return)

25

$200

$402,000

35

$200

$189,000

Difference

Same Investment

$213,000

5. Taking on Too Much Student Loan Debt

Excessive student loans can cripple your finances—another money mistake in your 20s with decades-long consequences.

The Student Debt Crisis:

Average 2023 graduate owes $37,000

Payments can exceed $400/month for 10+ years

Debt delays home ownership, marriage, and retirement savings

Smart Strategies:

Exhaust free money first (scholarships, grants)

Work part-time during school

Consider community college for gen eds

Choose federal over private loans

Explore income-driven repayment plans

Repayment Options:

Standard: Fixed payments for 10 years

Graduated: Payments increase over time

Income-Driven: Payments based on earnings

Refinancing: Lower rates but lose federal protections

Before taking out loans, optimize your cash flow. Our college budget template shows students exactly how to:

Uses actionable anchor text (“college budget template”)

6. Not Negotiating Salary

Underestimating your worth is a common money mistake in your 20s that can cost you hundreds of thousands over your career.

The Negotiation Gap:

70% of managers expect negotiation

Only 37% of young professionals negotiate

Not negotiating first salary can mean $1 million+ in lost earnings

How to Negotiate Successfully:

Research market rates (Glassdoor, Payscale)

Highlight specific achievements

Practice with a friend

Consider total compensation (bonuses, stock, flexibility)

Have a walk-away number

Negotiation Script:

“Thank you for the offer. Based on my research and [specific accomplishments], I was expecting something in the range of XtoXtoY. Is there flexibility in the offer?”

7. Relying Too Much on Credit Cards

Misusing credit cards is a dangerous money mistake in your 20s that leads to high-interest debt and financial stress.

The Credit Card Trap:

Average APR: 20-25%

Minimum payments barely cover interest

Can take decades to pay off

Smart Credit Card Use:

Pay balance in full each month

Use <30% of available credit

Choose cards with rewards you’ll actually use

Avoid cash advances (higher fees/interest)

Set up balance alerts

Debt Payoff Strategies:

Avalanche Method: Pay the highest interest first

Snowball Method: Pay the smallest balances first

Balance transfer cards (0% intro APR)

Credit card debt can spiral quickly—if you’re already struggling, our step-by-step debt payoff planner helps you escape the cycle with proven strategies like the avalanche method.

8. Skipping Insurance

Thinking you don’t need insurance is a risky money mistake in your 20s—one accident or illness can cause financial ruin.

Essential Coverage:

Health Insurance:

Employer plans

Marketplace options

Catastrophic plans for young adults

Renters Insurance:

Covers theft/damage

Often <$20/month

Auto Insurance:

Liability coverage required

Comprehensive for newer cars

Insurance Tips:

Compare quotes annually

Bundle policies for discounts

Increase deductibles to lower premiums

Understand what’s covered

9. Not Setting Financial Goals

Wandering without a plan is a major money mistake in your 20s—clear goals keep you focused and motivated.

Goal-Setting Framework:

Short-Term (1 year):

Save an emergency fund

Pay off the credit card

Medium-Term (2-5 years):

Save for a down payment

Pay off student loans

Long-Term (10+ years):

Retirement savings

Financial independence

SMART Goals:

Specific: “Save $5,000”

Measurable: Track progress

Achievable: Realistic timeline

Relevant: Aligns with values

Time-bound: Deadline

10. Falling for Get-Rich-Quick Schemes

Scams and risky investments are tempting but often lead to loss—another money mistake in your 20s.

Red Flags:

“Guaranteed” high returns

Pressure to act fast

Complex strategies

Unregistered sellers

Legitimate Alternatives:

Index fund investing

Real estate (REITs if no capital)

Side hustles with real demand

Career advancement

The Rule of 72:

Divide 72 by your expected return to see how long it takes money to double:

7% return = doubles every ~10 years

10% return = doubles every ~7 years

Final Thoughts: Building Financial Health in Your 20s

Avoiding these 10 money mistakes in your 20s puts you on the path to financial security. Remember:

Start small but start now – Compound growth needs time

Automate good habits – Savings, investments, payments

Educate yourself – Read books, take courses

Seek advice – Financial planners, mentors

Be patient – Wealth building takes decades

30-Day Challenge:

Week 1: Track every expense

Week 2: Open HYSA and retirement account

Week 3: Negotiate one bill/service

Week 4: Set 1/3/5 year financial goals

By making smart choices now, you’ll avoid regret later. Your future self will thank you for the financial foundation you build today.

If you are always running out of money and want to save some money, but you don’t know how it is time to start learning how to budget.

In this guide, we’ll discuss the essentials of budgeting for every stage of life.

Why Budgeting is Essential

Budgeting is more than just tracking expenses—it’s about taking control of your financial future. Here’s why budgeting matters:

Budgeting helpsAchieve Financial Goals

By developing a comprehensive spending plan, you can manage your resources effectively and ensure that each dollar contributes to your long-term aspirations.

Right budgeting canReduce Stress

Effective budgeting is a valuable resource for reducing financial stress. It offers a clear picture of income and expenses, allowing individuals to feel more in command of their financial circumstances.

Budgeting HelpsAvoid Debt

Effective budgeting is a crucial tool in preventing debt accumulation. By meticulously tracking income and expenses, individuals can better understand their financial landscape, allowing them to allocate funds wisely and prioritize essential expenditures. This proactive approach fosters responsible spending habits and creates a safety net for unexpected costs, reducing the likelihood of resorting to credit or loans. Ultimately, a well-structured budget empowers individuals to live within their means, paving the way for financial stability and peace of mind.

Budgeting is a factor in the Building Wealth

Effective budgeting is a crucial tool for building wealth. Individuals can pinpoint opportunities to save and invest more wisely by carefully monitoring income and expenses. This disciplined method enhances awareness of financial behaviors and enables people to make better choices regarding their spending and savings. With time, regular budgeting can result in substantial financial growth, helping individuals create a strong financial future and reach their long-term wealth objectives.

If you’re ready to take the first step toward financial freedom, this guide will show you how to budget effectively at every stage of life.

How Budgeting Can Turn You Into a Millionaire

Many people believe that becoming a millionaire requires a high income, but the truth is that smart budgeting plays a crucial role. By learning how to budget effectively, you can free up extra money to invest and let compound interest work its magic.

At just 18, Alex received a $100 birthday gift from his grandmother. Instead of spending it, he budgeted wisely and invested in a simple index fund, earning an 8% annual return. Inspired by his initial gain, Alex decided to invest just $200 per month, which he set aside through careful budgeting.

Fast forward to age 65—Alex’s investments have grown to an astonishing $2.1 million!

Meanwhile, his friend Chris, who didn’t learn how to budget early, waited until he was 30 to start investing the same $200 per month. By 65, Chris had only $650,000—less than a third of Alex’s wealth.

The difference? Budgeting for financial goals. Alex’s decision to prioritize investing through smart budgeting allowed compounding to do the heavy lifting. The key lesson: You don’t need a fortune to build wealth—just a solid budget and consistency.

What is a Budget?

A budget is a plan for your money. It outlines your income, expenses, and savings goals, helping you allocate funds wisely. Think of it as a roadmap that guides your spending decisions and ensures you live within your means.

Steps to Create a Budget

Creating a budget doesn’t have to be complicated. Follow these steps to build a budget that works for you:

1. Calculate Your Income

Start by determining your total monthly income. Include all sources, such as:

Salary or wages

Side hustles or freelance work

Pensions or Social Security

Scholarships or grants (for students)

Tip: If your income varies, calculate an average based on the past 3-6 months.

2. List Your Expenses

Next, categorize your expenses into fixed and variable:

Tip: Use bank statements or budgeting apps to track your spending accurately.

3. Set Financial Goals

Identify your short-term and long-term goals:

Short-Term: Saving for a vacation, paying off a credit card.

Long-Term: Buying a home, retiring comfortably.

Tip: Make your goals SMART—Specific, Measurable, Achievable, Relevant, and Time-bound.

4. Allocate Funds

Effective budgeting involves strategically allocating funds to ensure that resources are focused on the most important areas of need. This process requires evaluating different financial priorities and deciding how much money to assign to each category, including operational expenses, project investments, and contingency reserves. By thoroughly reviewing past spending and predicting future requirements, organizations can develop a balanced budget that addresses immediate obligations while also supporting long-term objectives. This careful distribution of financial resources is crucial for maintaining fiscal health and achieving overall success. See a paragraph below about the 50/30/20 rule.

5. Track and Adjust

Review your budget regularly to ensure you’re staying on track. Use budgeting tools or apps to monitor your spending and adjust as needed.

There’s no one-size-fits-all approach to budgeting. Here are some popular techniques to help you how to budget effectively:

1. The 50/30/20 Rule

This simple method divides your income into three categories:

50% Needs: Essential expenses.

30% Wants: Discretionary spending.

20% Savings/Debt Repayment: Future goals and debt reduction.

Tip: This method is ideal for beginners or those with a steady income.

Learning how to budget effectively can feel overwhelming, but online tools can simplify the process. A great resource is NerdWallet’s Budget Calculator, which helps you break down your income, expenses, and savings goals. By using a budgeting calculator, you can see where your money goes and make adjustments to ensure you’re on the right financial path.

2. Zero-Based Budgeting

With this method, every dollar has a purpose. Your income minus expenses should equal zero, ensuring you’re allocating funds efficiently.

Tip: Zero-based budgeting is great for detail-oriented individuals.

3. The Envelope System